Five years from now, you'll probably wish you'd started investing with Stock Advisor

Join over half a million premium members receiving:

- New stock picks each month

- Detailed analysis of companies

- Model portfolios and advanced tools

- Live streaming during market hours

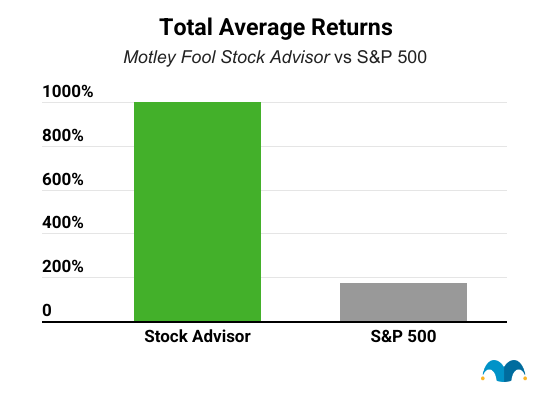

Stock Advisor Returns

+627%

S&P 500 Returns

+147%

Returns as of 04/26/2024. Stock Advisor launched in February 2002.

Featured Investing News

Got $1,000? 3 Stocks to Buy Now While They're On Sale

This Year's Top-Performing Dow Stock Is Down Over 8% In April. Is There More Pain Ahead?

Want $2,000 in Annual Dividends? Invest $30,000 in These 3 Stocks

3 Top Cybersecurity Stocks to Buy in April

Trending News

- Social Security's 2025 COLA Is on Track to Do Something It Hasn't Done For 15 Years

- Billionaire Bill Ackman Has His Sights on Only 1 "Magnificent Seven" Stock, and It's Not Nvidia

- The Vanguard 500 Index Fund Is Great, But Another Vanguard ETF Has Outperformed It the Past Decade

- Tesla Just Shared Some Spectacular News for Nvidia Stock Investors

- 1 Unstoppable Stock That Could Join Microsoft, Apple, Nvidia, Alphabet, Amazon, and Meta in the $1 Trillion Club

- 2 Roaring Growth Stocks to Hold for the Next 20 Years

- 1 Magnificent S&P 500 Dividend Stock Down 20% to Buy and Hold Forever

- History Says the Nasdaq Will Roar Higher This Year. My Top Growth Stock to Buy Before It Does.

- Tesla Sent a Clear Message to Wall Street on Tuesday

- This 15%-Plus-Yielding Passive Income Stock Continues to Deliver Despite Persistent Challenges

- Meet Eli Lilly's Secret Weapon in the Billion-Dollar Weight Loss Drug Market

- This Elite Dividend Stock Continues to Produce Powerful Growth

- Where Will Rivian Stock Be in 5 Years?

- One Member of Congress Is Going Against the Grain and Selling This Skyrocketing Stock-Split Stock

- 2 Fantastic Growth Stocks to Buy Right Now

Popular Topics

Best Stocks to Buy In 2024

Here are 10 stocks that could be excellent additions to your portfolio for the rest of 2024 and for years to come.

Top AI Stocks to Buy

Learn how you can make money investing in the wave of seasoned companies innovating in AI.

How to Invest in OpenAI & ChatGPT

Learn about the new AI chatbot dominating the internet.

6 Steps to Learn How to Buy Stocks

Here's a guide on what you need to do to get started with stock investing.

Top Marijuana Stocks to Invest In

The continued legalization of marijuana means growth for companies in this sector.

Best ETFs to Buy

Exchange-traded funds tend to be less volatile than individual stocks and provide portfolio diversification.

Top 3 S&P 500 Index Funds

Find out which index funds tracking the S&P 500 have the lowest fees and most closely track the market.

5 Top Hydrogen Stocks to Watch

A look at some of the leading hydrogen energy stocks that investors should keep an eye on.

High-Yield Dividend Stocks to Buy Right Now

A list of 20 high-yielding dividend stocks to consider buying now.

Dictionary of Financial Terms

The Motley Fool's list of financial terms. Making the world smarter, happier, and richer.

About The Motley Fool

Our Purpose: To make the world smarter, happier, and richer.

Founded in 1993 by brothers Tom and David Gardner, The Motley Fool helps millions of people attain financial freedom through our website, podcasts, books, newspaper column, radio show, and premium investing services. We believe that investing is empowering, enriching, and fun. We look forward to joining you on your journey to financial independence. Learn More

The Motley Fool Investing Philosophy

Learn How We Invest-

#1 Buy 25+ Companies Over Time

-

#2 Hold Stocks for 5+ Years

-

#3 Add New Savings Regularly

-

#4 Hold Through Market Volatility

-

#5 Let Your Winners Run

-

#6 Target Long-Term Returns

Investing Solutions Designed To Make Money Over The Long Term

Become a member today

Stock Advisor

Our base-level-membership giving you the foundation of a Foolish portfolio

Our Goal

Help members earn a positive return and build the foundations of a portfolio backed by Motley Fool principles.

Designed For

Individuals who are seeking easy-to-use guidance on investing in more familiar-named companies.

Recommended Minimum Portfolio Size

$5,000 +

Key Features

- Monthly stock recommendations (usually large and mid-cap stocks)

- Portfolio allocation guidance via The Motley Fool's Allocator tool

- On-going coverage of prior recommendations

- Access to Motley Fool Live video stream

Epic Bundle

A bundled membership that combines our four foundational stock-investing services into one

Our Goal

Help members outperform the benchmark by gaining exposure to a wider variety of stocks and investments.

Designed For

Individuals who are regularly adding new money to their brokerage accounts, interested in business, and want to spend more time learning the art of investing.

Recommended Minimum Portfolio Size

$25,000 +

Key Features

- Includes access to Stock Advisor + Rule Breakers + Everlasting Stocks + Real Estate Winners

- Weekly stock recommendations (ranging from small to large-cap stocks)

- Portfolio allocation guidance via The Motley Fool's Allocator tool

- On-going coverage of prior recommendations from all included services

- Access to Motley Fool Live video stream